Publisher’s Note: This is an extract from The Outperformers: Lessons from Top Law Firm Leaders by Kent Zimmermann, Patrick Smith and Carlyn Kolker, published by Globe Law and Business. The Texas Lawbook is hosting a lunch conversation with Kent on Tuesday, June 2 at noon discussing the book and legal market trends. Please email brooks.igo@texaslawbook.net if you are interested in attending.

A RAPIDLY CHANGING COMPETITIVE LANDSCAPE

1. Introduction

Consider a patient who needs specialised heart surgery. He or she wants a surgeon who is known as the best, or among the best, and who performs that work all day, every day, backed by a hospital with deep expertise and the resources to match. That hospital will be the leader in its field, and will be in high demand for the specialised heart surgery, drawing graduates focused on the same discipline who clamour to train there.

Now, apply these same advantages of market leadership, particularly at scale, to law firms. A law firm benefits from a deep bench of partners who are recognised as leaders in areas for which the firm wants to be known as the best, or one of the best.

This reputation attracts both talent and clients: lawyers want to learn from the best, and clients shortlist firms dominant in particular areas. As demand increases, the firm is in a position to hold rates firm and increase them more rapidly than competitors, particularly in areas of practice experiencing growing demand. The result is a virtuous circle: market leadership drives increased demand, increased demand justifies premium rates, and profitability funds investment in the firm’s people to defend or enhance its leadership position.

2. Growing Differentials

Almost all law firms are confronting a growing differential in both size and profitability relative to their competitors, and in recent years a small cohort of high-performing firms have pulled away from the pack at the top of the market.

As outperforming law firms grow in size and profitability, their relative ability to attract and retain needle-moving lawyers often expands. Over time, this creates substantial gaps in capability, depth of bench strength and market competitiveness between firms that were once similar.

Alden Millard, the chair of New York-based Simpson Thacher & Bartlett, comments as follows:

“I think a lot of the change in the industry is because there used to be a manageable differential between one firm and another firm that was a little bit bigger and higher performing. But as the differential grows, it becomes imperative for firms to do new things.”

3. Size Differentiation

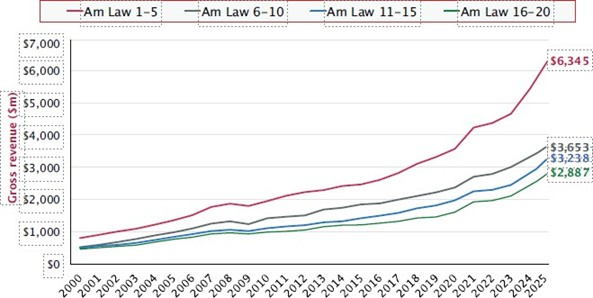

Two law firms in particular, Kirkland & Ellis and Latham & Watkins, are frequently cited for having reshaped the dynamics of revenue and profit growth, and now consistently take the top two spots on The American Lawyer’s list of highest-grossing firms, while also consistently being among the most profitable. Those firms unseated the prior leaders on size from the 2000s and early 2010s, such as DLA Piper, Baker McKenzie and Jones Day.

Latham & Watkins first topped the Am Law 100 gross revenue rankings in the 2015 list. Then, two years later, Kirkland, with deep roots in the private equity sector, topped the list – a position it has held ever since – including in the latest rankings published in 2025, when it reported nearly $9 billion in gross revenue. Both firms are now achieving at least 1.5 times the revenue of their nearest competitors.

Other firms that have steadily climbed the Am Law 100 ranking, such as Ropes & Gray and Sidley Austin, have been propelled by premium work in powerful asset classes, including M&A and fund formation, as well as deal work for private equity and private credit firms.

Figure 1: Growing delta among Am Law 20 firms in gross revenue segments

Several firms with high gross revenue and headcount also boast high profitability. In contrast, in previous decades, firms that ranked high on the Am Law 100 list of highest-grossing revenue firms were not necessarily among the most profitable.

Firm leaders, particularly those in historically stable, venerated, Wall Street-centric firms, often operated on the assumption that firms had to choose between profitability and size. However, more recently, a cohort of large and rapidly growing firms have turned that notion on its head. These firms have simultaneously expanded their headcount and gross revenue, while also increasing their profitability, some to levels that would not have sounded plausible just a few years ago.

Many of these fast-growing firms are adding to headcount in high-revenue and profit-producing markets. For example, the majority of the most profitable firms are based in New York or have grown their New York offices to be their largest.

Latham & Watkins surpassed 800 attorneys in its New York office, more than 2.5 times as many as it had in its founding city, Los Angeles.

Kirkland & Ellis, founded in Chicago, surpassed 1,000 lawyers in New York, making that office more than 20% larger than its Chicago office.

4. Profitability Gap

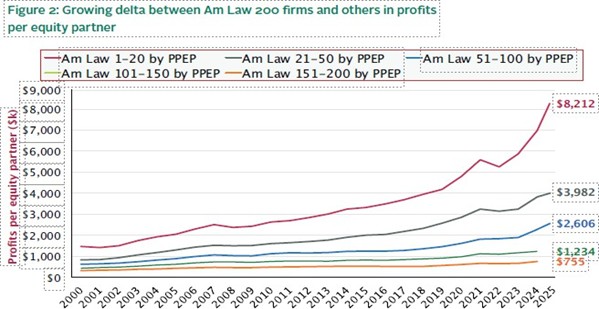

We also continue to observe a notable differential between Am Law 20 firms and other firms, as measured by profits per equity partner. Outperforming firms have shown a combination of approaches to growing their profitability.

Some firms focus their time and money on clients willing to pay premium rates, and leverage their strengths, particularly in areas of growing demand in which they can credibly become a market leader or defend their position as one, thereby adding to their ability to drive outsized revenue and profitability growth relative to other firms, all things being equal.

Some create a tier of non-equity partners, helping to retain the best associates without making them equity partners; cull underperforming partners with discipline; and pair strategic headcount growth with ambitious rate increases.

Some pick up the pace on strategic growth with groups of laterals.

And some firms do all these things and more, as we will explore.

5. Increasing Stratification

A trend of increasing stratification is becoming evident even among the most profitable firms. Some firms – call them ‘the elite of the elite’ – are pulling away from the pack. There is a growing gap in profitability between the elite performers and the next tranche of high-performing firms.

Figure3: Gap between the top five most profitable firms and the next five firms, as measured by PPEP

A fundamental truth emerged from our work and the input we received from leaders of outperforming firms: most have no desire to become a different firm, but they do aspire to be a stronger version of themselves.

6. The Magnet of Outperformance

Simply put, outperformance relative to direct competitors for talent enables firms to more often attract more desirable lawyers and clients. Market dominance creates a strong magnet for sought-after clients, work and talent. Given that outperforming firms have comparatively greater resources to invest in talent, more ability to leverage their deeper bench, and the capacity to make larger capital investments, these firms are well positioned to ascend to ever greater heights, making them hard to keep up with.

To provide a data point, many high-performing firms invest 1% of their gross revenue annually in capital expenditure – referred to in some firms as R&D – focusing on:

- technology and innovation broadly;

- leveraging the firm’s knowledge and other information;

- data analytics;

- practice leadership development; and

- broader talent development.

One per cent of $500 million is $5 million; of $1 billion is $10 million; of $3 billion is $30 million; and of $9 billion is $90 million. These are substantial annual investments.

7. Specialisation

General counsel and business leaders who select outside firms report in surveys that they frequently turn to just a shortlist of firms for board-level matters in whatever areas of legal expertise they need, whether that’s high-stakes transactional, litigation or regulatory work.

This creates potential advantages for firms in prioritising growth in certain practices, sectors and cities. For example, it may mean focusing on certain sub-areas of high-stakes litigation, such as mass tort litigation and certain transactional matters, including large-scale M&A, to meet the seemingly insatiable needs of private equity and alternative asset funds to deploy capital and generate higher returns.

In addition to Kirkland and Latham, other highly profitable firms that have differentiated themselves in these areas include Paul, Weiss, Rifkind, Wharton & Garrison, Proskauer Rose and Sidley, to name a few – all firms whose rates of growth in revenue and profitability over the last decade have exceeded the norm.

This work is also driving firms to merge or look for acquisition opportunities to accelerate achievement of their goals on size, profitability and market leadership in chosen areas. McDermott Will & Emery’s 2025 merger with Schulte Roth & Zabel – a firm with deep ties to hedge funds and private capital clients – to become McDermott Will & Schulte, is one of the latest and highest-profile examples of how firms are thinking big, and fast forwarded the achievement of their aspirations with inorganic growth.

8. Vulnerabilities

Firms that have slipped on a relative basis, allowing a growing gap in size and profitability compared to competitors, have less flexibility on compensation, making them more vulnerable to losing key partners, which can in turn trigger a loss of independence.

A trickle of high-performing partners departing can become a stream, sparking a crisis of confidence in leadership. Such crises are a common thread in the narratives of firms that experienced reversals of fortune, lost their independence or dissolved.

In New York, for example, firms that lost their independence in recent years suffered from this growing differential in size and profitability relative to their closest competitors. These included Stroock & Stroock & Lavan (now dissolved), Shearman & Sterling (now A&O Shearman following its 2024 merger with Allen & Overy), Kramer Levin Naftalis & Frankel (now Herbert Smith Freehills Kramer following its 2025 merger with Herbert Smith Freehills), and Schulte Roth & Zabel (now McDermott Will & Schulte following the 2025 merger referred to above).

A similar story played out earlier in Texas, where national and multinational firms that leveraged size and profitability advantages poached needle-moving partners from regional players in the late 2010s and early 2020s, resulting in a loss of independence for firms such as Gardere Wynne Sewell (now part of Foley & Lardner following their 2018 merger), Thompson & Knight (now Holland & Knight following their 2021 merger), and Andrews Kurth Kenyon (now Hunton Andrews Kurth following its 2018 merger with Hunton & Williams).

While each firm’s transition has its own unique story, all suffered from major and growing gaps in scale and profitability compared to larger competitors. This made it difficult for them to match compensation levels and invest sufficiently in the future of their firms, and ultimately reduced their appeal to both talent and clients.

A firm that is performing well in isolation may still be weakening within the competitive landscape. Relative comparison is essential, given that firms are competing for talent. The cost of staying the course or doing nothing differently – even when a firm is improving in absolute terms – can be substantial.