© 2017 The Texas Lawbook.

By Natalie Posgate

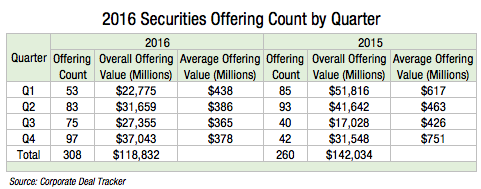

(May 3) – Texas corporate securities lawyers handled 19 percent more securities offerings in 2016 than they did the year prior, but their 308 capital markets transactions raised 16 percent less cash, according to new data from The Texas Lawbook’s Corporate Deal Tracker.

The 2016 results point to an influx of smaller and mid-sized energy companies rushing into the capital markets, which suddenly reopened to them halfway through the year after a stagnant year-and-a-half caused by the energy downturn.

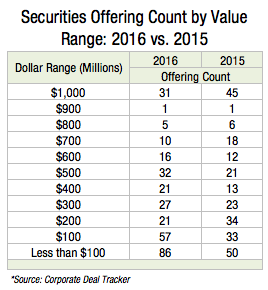

The data also shows a steep decline in “mega” offerings by larger companies. Texas-based attorneys handled 31 percent fewer securities offerings valued at $1 billion or more in 2016 than they did in 2015.

Conversely, securities offerings that raised under $200 million saw a 72 percent spike, and those that raised between $400 million and $600 million increased 56 percent.

The uptick of deals in those value ranges indicates a renewed sense of optimism for the small- and mid-sized energy companies that drive dealflow in the economy. But it also demonstrates the heightened caution investors took with larger oil companies through most of 2016 as the market began to recover.

“Investors were being more cautious about how they wanted to put money to work in the energy industry,” said Mike O’Leary, a partner at Andrews Kurth Kenyon in Houston. “They were not as willing to put huge amounts of money to work. The larger offerings were healthy companies that needed to raise capital, and the investor appetite was there – companies with a good reputation and a good story that would convince investors it was worth the investment.”

The Corporate Deal Tracker data includes public and private debt and equity offerings led by— or significantly handled by — Texas-based attorneys.

The revival in work comes after a god-awful rut in securities offerings that began halfway through 2015 as oil prices continued to tank and hit lows the market had not witnessed for over a decade.

Thus, the Corporate Deal Tracker data and capital markets legal experts point to a stabilization in oil prices as the main driver for the increased securities offering activity. About 82 percent of all offerings reported to the database last year involved energy companies as the issuers.

“In early 2015, we were surprised by how much capital markets activity there was,” O’Leary said. “It was both companies rushing at a time when they needed capital, as well as investors who thought the worst of pricing had been seen, that there was more of an upside than a downside. By mid-2015, they realized that was wrong.

“The way the years fell were completely opposite of one another,” he added. “2015 had a strong first half; 2016 had a weak first half. There were almost no offerings, and certainly no IPOs. All were follow-on offerings by companies.”

That turned around halfway through 2016, when oil prices began to stabilize and hover around $50 per barrel.

“I think it was about May of 2016 when things looked more optimistic, and the prices began to firm and rise,” O’Leary said. “As prices firmed in the summer of 2016 and began to look like they weren’t going to slide again, OPEC was able to reach an agreement to restrict production, and that really helped the market. It helped investors have the confidence to come back to the energy market.”

The data speaks for itself. The best quarter of 2016 was the fourth, which began a few days after OPEC agreed to cut oil production. The 97 securities offerings that Texas lawyers reported to the Corporate Deal Tracker in Q4 demonstrated a slightly stronger market compared to 2015’s best quarter, the second, which saw 93 offerings.

Offering count escalated even more throughout December after OPEC finalized the deal to cut output on Nov. 30. The 43 securities offerings Texas lawyers worked on in December accounted for 44 percent of the 97 offerings reported in the fourth quarter.

As a bonus, companies began successfully completing more initial public offerings. Of the 11 IPOs reported to the Corporate Deal Tracker in 2016, six occurred in the fourth quarter, and one occurred late in the third quarter.

“At the end of 2016, we really started to see what I consider a return to normal,” said Sean Wheeler, a partner at Latham & Watkins in Houston. “Right now, there is a lot of excitement about IPOs. I’d say what has been exceeding my expectations is the number of people seeking to go public in the energy space.

“A number of companies spent the downturn building their business in anticipation for the rebound,” he added. “As soon as the rebound occurred, they made an effort to move into the public market.”

Because a heightened IPO presence in any industry reflects a sense of optimism and growth in that market, capital markets lawyers are excited for what’s ahead in 2017. The IPO revival could also lead to other kinds of capital markets work, they say.

“Typically a healthy IPO market also suggests a healthy follow-on equity market,” said David Oelman, a Houston-based partner at Vinson & Elkins.

Oelman and others are already seeing a sharp increase in IPO work this year.

“I think we’re working on 10 IPOs that have been publicly filed, and twice as many that are in various stages of gestation,” Oelman said.

Just this past week, Oelman and fellow V&E partner Alan Beck closed a $122 million IPO for Select Energy Services, a Gainesville, Texas-based oilfield services company backed by New York private equity firm Crestview Partners. Oelman also has IPOs in the works for Liberty Oilfield Services and the underwriters of Antero Midstream GP LP.

2016 offerings: the anatomy

Beyond sheer volume, the types of offerings that Texas lawyers worked on greatly differed between the first half and second half of last year.

Aside from the fact that very few offerings got done in early 2016, the ones that did illustrated the strain or uncertainty that some companies were feeling – particularly the equity deals.

At the beginning of 2016, many of the equity offerings companies issued were for “defense reasons,” like “shoring up their balance sheets,” Oelman said.

While some upstream companies were participating in these kinds of issuances, Oelman said he saw even more of his midstream master limited partnership clients partaking in this offering trend. Typically, the transactions entailed issuing preferred stock – usually through a private placement, since at the beginning of the year the capital markets were still widely closed to companies. Among these offerings were Plains All American, MPLX and Western Gas Partners, which raised $1.6 billion, $1 billion and $702 million, respectively, during Q1 and Q2 2016.

Before IPOs made a comeback, the offerings that were public were often follow-on equity offerings or debt utilized to improve companies’ balance sheets or to fund opportunistic acquisitions of other businesses.

“It was still a busy year, but the type of work was different than previous years,” Wheeler said.

Now that IPOs are coming back, the participating companies are predominantly upstream and oilfield services.

There are a number of upstream companies that are engaged in the IPO process, particularly natural gas-focused companies in the Haynesville shale,” Wheeler said. “It just seems that every oilfield services company wants to go public – every oilfield services company that exists. I’d suspect a good number would be just as happy with an M&A exit.”

Legal experts clarified that the upstream and oilfield service companies going public are in the form of C corporations – not MLPs, which was a trend in 2014.

“The downturn that we’re just emerging from… showed that upstream MLPs and oilfield services MLPs don’t do well in the type of MLP structure where you have quarterly distribution rights,” O’Leary said. “If they have variable distributions, they can do well. Many investors lost an awful lot of value in those companies.”

The only MLPs that are going public are midstream companies, though not to the level oilfield service and upstream companies are going.

The one MLP midstream IPO that closed last year was Houston-based Noble Midstream Partners. It was also the first energy IPO in general to successfully close in 2016. O’Leary led the IPO for Noble.

“When Noble Midstream’s IPO got done in the fall, it really helped show that investor appetite was there for strong sponsor-backed midstream MLPs again,” O’Leary said.

Following the money

When the 2016 offerings were dissected into value ranges, the winners were small and middle-range values and mega-offerings were the losers. Securities offerings valued at $1 billion or higher declined by 31 percent from 2015.

The low stock value of companies across all facets of the energy industry could have contributed to the downturn of larger offerings that took place in 2016, Oelman said.

“Companies wanted to raise as little money as they could to serve their needs,” he said, especially “if your CEO or shareholders asked why you’re selling stock when it’s trading at an all-time-low.”

Offerings valued between $400 million and $600 million, on the other hand, increased by 56 percent. Smaller offerings, or those valued below $200 million, increased even more in 2016 – 72 percent. And offerings that raised below $100 million comprised more than one-fourth of all offerings reported to the Corporate Deal Tracker in 2016.

During the downturn, smaller energy companies had more trouble raising cash because since they were smaller, they were “less financially stable, so their access to capital was cut off even more” than larger companies, Wheeler said.

“I think the fact that smaller offerings have increased makes a lot of sense to me given the fact that a larger group of companies have more access to the capital markets than they did a year or two ago,” Wheeler added.

Though the overall value of offerings was higher in 2015, bigger transactions didn’t always mean better. The data was substantially skewed by two mega-debt offerings that added $13.5 billion to – and accounted for 10 percent of – 2015’s overall $142 billion value. Both were public offerings of senior notes for Halliburton and Schlumburger, two companies in the segment of the energy sector that was hit the first and the hardest during the oil price downturn: oilfield services. (At the time, both were also the acquiring parties in two mega-mergers, albeit only one successfully closed.)

“They needed to raise money to pay their bills, and their revenues were going down dramatically,” said Oelman who was not involved in either offering. “They couldn’t borrow more money, so they had to execute a debt financing operation because expenses were higher than revenues… They may have maxed out on their credit facility.”

Had those two offerings not occurred, the value decline from 2015 to 2016 would have only been 8 percent instead of 16 percent.

The largest offering reported to the database in 2016, on the other hand, was Anadarko’s $3 billion offering of senior notes.

© 2017 The Texas Lawbook. Content of The Texas Lawbook is controlled and protected by specific licensing agreements with our subscribers and under federal copyright laws. Any distribution of this content without the consent of The Texas Lawbook is prohibited.

If you see any inaccuracy in any article in The Texas Lawbook, please contact us. Our goal is content that is 100% true and accurate. Thank you.